Britain’s most famous high street retailer “M&S”, which has been going round in circles for years trying to fix its ailing clothing business, has come up with a solution which has embroiled them in a dispute. M&S is consulting staff over the axing of premium pay on Sundays, and cuts to the pay for bank holidays and for employees working anti-social hours. This potentially affects around 7,000 staff. It also plans to reduce pension contributions, which would hit 11,000 employees.

As per them, despite these changes it will allow the chain to deliver “some of the highest wages in retail”, while the pension changes will deliver “parity” to all employees. The employees who would not agree to the new contracts will be sacked. This is more troublesome for the staff because if they agree to this contract their monthly income in hand will be reduced and if they don’t agree they would be losing their job.

As a result of Britain’s fast-changing and ruthlessly competitive marketplace, many retailers are struggling to survive. According to the British Retail Consortium (BRC), a trade group, sales growth has been slowing since early 2015. There have been some prominent high-street casualties this year, such as Austin Reed, a menswear brand, and BHS, a chain of department stores.

So is the pay row justified? From a business stand point, pay cuts give M&S some leeway to turnaround without having to fire people, especially the ones who have spent years with the company. So it should be a sentiment that employees appreciate, right? But this is not going down well with the workers especially ones who have been with the company for a long time. From the stand point of the employees reduced pay would mean a shortfall in meeting monthly expenses. This in turn could drive most of the workers to borrow money either through payday lenders or other expensive sources. So it is a double whammy for them – reduced income and increased debt.

Can this gap be filled? Credit Unions in their partnership with FairQuid can help bridge some of this gap. Since in the FairQuid model the length of service with the company and payroll deductions are key factors to reduce the associated risk for the credit unions. So in effect the employees can use their length of service with the company and negotiate better terms on their borrowings. The money saved through this can help bridge the gap that is left in the income without it costing anything direct to the company.

In all it will be a win-win-win situation for all the 3 parties: 1. Company: It will have a chance to do a recovery and save jobs 2. Employees: Instead of using just their credit score with expensive lenders, they can get to use their length of employment for fair term loans 3. Credit Unions: Success in their mission of providing alternative ethical credit in the UK economy

Leaving the European Union is a substantial step for any member state to take. The decision is in many ways a social, cultural and political one, but it is also one which carries economic implications. The United Kingdom’s decision to leave the European Union, or ‘Brexit’, has consumed much debate. The magnitude of the economic costs and benefits of Brexit cannot be known with certainty before the event. The unexpected result of the vote and its ensuing fallout has created an atmosphere of instability and ambiguity, which never bodes well for the economic climate.

As per the data from Adzuna, a job-search website, their count of new job ads put up was 29,000 compared to 39,000 (This is week on week number), a worryingly large fall of 26%. The count of new ads over the past seven days is 570,000, compared to 615,000 the week before (a 6% fall). Employers, it seems, are already less keen on hiring. Many companies opt for stack ranking (also known as “20-70-10” system) of employees in this situation, which creates job insecurity and demotivation among the workers. The workers are divided into “A” (20%), “B” (70%) and “C” (10%) players, where A being the top performer, B the vital majority and C being the poor performers. The “C” workers are let go as management feels this way they can kill two birds with one stone – 1. Reduce workforce costs ahead of tough time, 2. Avoid letting go of the vital majority for some time. However as the workers are not told their ranking, it creates a sense of job insecurity among “A” and “B” players as well, since they feel they would be the ones in the next round.

As a result, “A” performers start leaving as they are in a position to secure alternative jobs even in a tough economy. So the business is in some ways stuck with “B” players as they do not find jobs as easily in the tough market but with the insecurity and de-motivation their productivity drops and can very quickly become “C” players. So very easily the companies can be left with “C” players that they were trying to reduce to begin with.

When you force employees to fit into a pre-determined ranking system, you do three things:

1) Incorrectly evaluate people’s performance, by forcing line managers to fit their teams in the 20-70-10 bell curve model

2) Make everyone feel like a number, and

3) Create insecurity and dissatisfaction when performing employees fear that they’ll be fired due to the forced system.

This flux and uncertainty of Brexit is an opportunity for the HR professionals to not be reactive but be proactive. As an HR professional if you are proactive then you not only prevent “A’s” from leaving but also motivate “B’s” to become “A” players. You should consider that people have responsibilities toward their families and they have bills to pay every month. The best reassurance and benefit one can provide in these tough times is the freedom from financial distress.

It is time for companies to start focusing some of their HR efforts on tackling financial stress. With the new breed of employee benefit offering money management tools; it’s now possible to do this effectively and in a targeted manner. Employers should tie up with financial employee benefit providers like FairQuid that provides access to savings and affordable loans through local Credit Union partners. The employees irrespective of their salary scale just have to fill in the loan application form online from the convenience of their office desktops. The saving contributions and repayments are automated through payroll deductions; therefore they don’t have to worry about missed repayments. Since Credit Unions are providing this facility based on their employment and length of service with the company, it encourages the employees to stay with the company till the loan is repaid and thus helps directly reduce the turnover rate in the short term. Thus FairQuid, through its Credit Union partners, provides financial freedom to one and all irrespective of their income.

Giving employees the tools for financial resilience can break the needless spiral of anxiety and stress. This is crucial as far as productivity is concerned, where the impact of financial stress on the workplace can be dramatic.

Low financial capability and resilience is and has been a significant cause of stress across the UK workforce. These money worries have a clear impact on their productivity at work and attrition rate.

Employers always have an impact on the financial wellbeing of their workforce as the primary source of income for most people. The answer isn’t just higher levels of pay. Instead, employers need to help their staff learn healthy financial behaviours and build financial resilience.

According to a survey by SMF, One in five people (19%) think they are now under less financial pressure than they were two years ago. But twice as many people (40%) feel that they are now under more financial pressure. A third of people (32%) are fairly or very concerned about the level of debt they have at the moment and Four in ten workers (38%) say money worries have made them feel stressed. These worries have a clear impact on how people feel and behave as they go about their day-to-day life and work.

An individual’s financial wellbeing is inextricably tied to their workplace. As per Conclusion of the workplace report, Barclays Corporate & Employer Solutions and Barclays Workplace Banking, May 2014.

• 46% of British workers are struggling with their finance • 70% have little or no savings at all

Employers will necessarily impact on the financial wellbeing of employees, whether they intend to or not.

What Employers can do to improve employee’s financial stress?

• UK employers must now offer a workplace pension to all employees. These pensions must be offered on an opt-out basis – that is, the employer will automatically help the worker save for their retirement by putting away a small proportion of their salary, unless they specifically decide not to participate. • Auto-enrolment into income protection policies. By providing insurance cover for those times and individual is unable to work due to ill health or family problems, these policies can help to smooth income in the same way as savings. • Providing budgeting tools alongside online payroll services could help employees to make better decisions with their money. • Employers could also consider directing their workforce to online financial aggregator platforms, which help consumers to see all their financial assets and obligations in one place and to track their spending. • Employer should tie up with financial employee benefit providers to provide access to affordable loans to the workforce via ethical lenders like Credit Unions • Enable employees to borrow money through workplace benefits at a competitive rate.

Provision of simple tools could also help employees to take control of their money. Together, these steps taken could help the UK workforce to move to more sustainable forms of credit, grow their savings and avoid the stress of money worries which in turn would mean that people will not frequently change their job for more compensation and would lead to reduction in attrition rate.

When you start a new business typically you are focussing on idea validation, market validation, product validation to begin with. Very soon you move on to market sizing, revenue and expense forecasting, cash flow models to ensure you can not just grow fast, but survive too. Go-to-market plan execution then consumes you.

In all of this the thing that makes it all worthwhile and gives you the stamp of approval, is feedback on how you have actually made a difference in someone’s life.

Feedback like this (reproduced below) is what makes us go Yayyyyyy!!!

“Just a quick mail to say thank you for helping me out with this work based loan!

This has helped me out massively. Trying to look after three kids and day to day bills I found myself in a hole and felt I had nowhere to turn. I was maxed out on two credit cards, one with a limit of £3500 and the other £1000. My Vanquis card had an interest rate of 39.9% APR and the Halifax had a 18.9% APR. Some months my outgoings on these credit cards amounted to around £200 and this was just in interest alone! At this point no matter how hard I tried I felt this was never going to be paid. I tried looking into other loans to pay these off in full but was declined.

Thanks to this scheme I have been able to borrow £4000 and with some help from my first wage I have manage to pay both credit cards off in full. Both of these cards have now been cut up and cancelled to avoid falling back into the same situation. I now have one manageable payment of £280 for the next 24 months. The fact this comes straight out of my wages on payday makes it so much better for me as I don’t miss it. Knowing in 24 months I will be debt free and also will have accumulated £240 in savings is a huge weight lifted from my shoulders and for that I thank you!” a FairQuid user

FairQuid, a new employee benefit loan scheme which promotes employees’ financial wellbeing, has recently exited its trial period and been officially released to the Lancashire business community.

Initially launched and trialled at 645-strong Darwen based manufacturing company WEC Group Ltd, the scheme aims to improve employee engagement and retention by offering access to low cost borrowing and improved money management practices through the use of local community Credit Unions.

Challenged with a high staff turnover (>20% p.a), WEC Group Commercial Director Wayne Wild was looking for an employee benefit that would attract and retain talent. He was convinced that Credit Union membership could be a huge benefit for his employees, so he worked with the Jubilee Tower Credit Union in Darwen (who were recently awarded the Publisher’s Award at the Red Rose Awards 2016) and became co-founder of FairQuid as a solution. Within one year of implementation at WEC Group, FairQuid achieved its goal of improving staff retention well above expectations. Over 130 employees joined the scheme within the first few monthsand over £140,000 of high interest debts have been refinanced through Jubilee Tower Credit Union.

Staff turnover dropped to under 4% for those taking advantage of the scheme, saving the business over £240,000 in recruitment and associated staff replacement costs.

As a simple, fair, and responsible framework, employees can apply for a short term loan from their local credit union through an online platformprovided by FairQuid. Criteria is based around their salary, service level and employee record, and a maximum of 20% of an employee’s annual salary is the loan value which can be applied for. Repayments are automatically deducted from the employees wage within a set period of a maximum of 24 months meaning no payments can be missed.

The success of the scheme is mostly due to the fact that FairQuid encourages a responsible pay back method with set repayments through payroll deductions. No roll over borrowing is possible in accordance with the ethical rules of Credit Unions, which are not-for-profit organisations operating savings and loans accounts for their members. Wayne commented: “It’s a win-win-win. The employer wins by saving on retention and recruitment, and staff win with access to low-cost borrowing and improved sense of money management.”

FairQuid also offers many benefits to Credit Unions as it helps them acquire new members, increases fund development and improves their portfolio quality. In addition, it enables employers to improve productivity and decrease staff turnover, which on average costs companies 4% of their bottom line.

Wayne Wild continues: “All loans are provided by the local credit unions and repayments are made through payroll deductions, meaning there is no strain on your company’s cash flow. We have no liability for the loans which makes it a great staff benefit for WEC Group at absolutely no cost to us.”

Following its success, FairQuid was officially released to other North West businesses at a recent Lancashire HR Employers Forum in Preston with strong interest recorded on the day. The company is now actively promoting the scheme to other organisations who are interested in helping employees improve their financial wellbeing.

A number of Credit Unions in Lancashire, Cheshire and Yorkshire have already joined the scheme, enabling FairQuid to increase their catchment area further. Discussions are already in place with other credit unions and employers nationally.

Employee benefits are increasingly popular and we frequently hear about this new high tech start-up that offers unlimited holidays, stock options or discounted travel tickets. All these perks sound great on paper but do they have a real impact on staff motivation and retention, if your company is not Uber or Virgin and you don’t have a workforce made of 25 year old computer geeks? In a recent study on employee wellbeing* Barclay’s highlights the employee benefit disconnect where 72% of employers are confident they provide a good benefit package but more than 78% of employees disagree.

Two main factors can account for this strong discrepancy: 1. Chasm between benefits offered and needs of your employees 2. Communication on benefits available to the employees

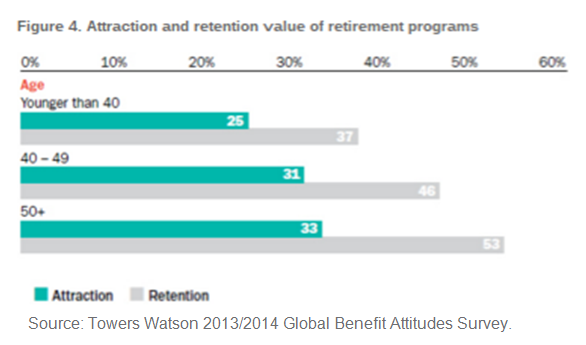

Chasm between benefits offered and needs of your employees For your employees to commit to your company goals, and go the extra mile, to make sure that they are achieved, the very first thing that comes to mind is, for you to go the extra mile for them. Get in their shoes and see what challenges they face in their daily lives. Create an ecosystem where they can focus on work and not have others worries occupying their minds. Maybe a good way to evaluate benefit packages could be to go back to basic concepts and compare what needs you’re satisfying on a Maslow Pyramid and where your employees actually stand on this scale. 1. Physiological needs 2. Safety 3. Love/Belonging 4. Esteem 5. Self Actualization In a developed economy, like UK, one would expect all people to rank high in Maslow hierarchy of needs. While physiological needs are mostly covered, the need for safety (financial) is often not entirely fulfilled. Living in a stable and predictable environment is an essential feature that your employees look for. Several benefits exist and the most famous are healthcare and retirement plans. While these benefits are attractive to 40+ y/o employees, their impact on younger staff is far less significant.

According to Barclay’s Study, 40% of UK citizens have less than one month’s savings and make attractive business for loan sharks (payday lenders and credit card companies). How could your employees be engaged and focus on work when they lose sleep at night, because they don’t know how they are going to pay their bills or fund an unexpected expense? Employees don’t leave their financial issues and stress at the door, when they come to work in the morning. Salary increases and company lending are not viable options. In a competitive environment a few percent raise in salary has little to no real impact on employee’s well-being but can be enough to wreck an organisation’s finances. That’s when smart benefits come into play; to implement benefits that will be adapted to the specific needs of your employees and sustainable for your company. Employee financial health is probably the most significant area for HR managers to focus on, but there are many more. HR managers are key to assess what employees need, to deliver their full potential for the greater good of the company. They are also responsible for its successful implementation which can’t happen without a full commitment from the HR team.

Communication of your benefit package For a benefit package to succeed within the company, HR managers must support it actively. Regardless of whether the benefit package was tailored at the company or purchased from a benefit provider; HRs are the key to massive employee adoption of any benefit package. If HRs don’t actively support and promote it, it will not be successful no matter how good it is for employees. Communication tools exist and can be used to set up active long term promotion campaigns. Some ideas: – Common advertising: posters, leaflets – More advanced advertising: company internal meetings, newsletters, visibility on intranet, case studies & employee feedback – A benefits portal with easy access online 24x7x365

Being seen is not enough. Make sure your benefit package is easily available and enrolment is hassle free and convenient. The interface is key: Thaler and Sunstein showed in Nudge# that the interface determines the behaviour of people. Let me give you a very basic example. At a company/school cafeteria depending on how food items are arranged you can increase or decrease the consumption of any food item up to 25%. This experiment is a good illustration of the Nudge theory. In other words, how you can influence healthy behaviours through the choice interface you’re offering to your population. In the employee benefit area this theory was implemented in the US as suggested by the Save More Tomorrow program where employees monthly retirement savings contribution is automatically raised every time they got a pay raise unless employee logs in and cancels the automatic raise in his monthly salary deduction. In its first implementation, the Save More Tomorrow program helped boost the average participant’s 401(k) savings rate from 3.5% to 13.6% in just 3.5 years. People want to save more but they just don’t have the reflex to do it. Save More Tomorrow nudges them to increase their savings and lets them free to do otherwise if they don’t want to.

As we said retirement plans are good ideas but not enough to retain all workers that might be focusing more on the present rather than on their retirement strategy. In the UK, there is the example of Credit Union^ payroll deduction schemes. They are great opportunities for employees to get back on track with their finances by having access to affordable and healthy lending and a strong incentive to save money every month. However, very few employees join Credit Union payroll schemes because of lack of convenience and user-friendliness: the interface is just not right. – Credit Unions only lend to members (with at least 3 months or greater membership history) but usually people only think about joining when they need a loan. – Plus, even if your company has a payroll scheme with the local Credit Union, you still have to mail documents or show up physically at their local office. – So people end up going online to payday lenders or using credit card debt even if it is more expensive and they can’t afford it, but it is convenient, quick and easy.

WEC Group a Lancashire-based metal fabrication company is one concrete example of how understanding the Nudge effect and optimizing the user interface can dramatically increase employee adoption of a new benefit. WEC had a payroll deduction scheme with Jubilee Tower Credit Union but uptake from employees was not that encouraging. One of the directors, Wayne Wild was challenged with a high staff turnover (>20% p.a.) and was looking for a benefit that would attract and retain talent at WEC. He was convinced that Credit Union membership could be a huge benefit for his employees. He decided to change the way employees accessed Jubilee Tower Credit Union Services and introduced FairQuid Employee Benefit scheme. This innovative idea was a game changer as it made it easy and hassle-free for employees to get the loan they needed at a fair rate of interest. No need to save before they borrow and everything happens online in real time. 1 year after implementation the scheme has achieved its goal of improving staff retention above expectations. Over 130 employees have joined the scheme and staff turnover dropped to 4%, saving the business over £250,000+ in recruitment and associated replacement costs.

“It’s a win-win,” says Wild. “The employer wins by saving on retention and recruitment; staff win with low-cost borrowing. The only thing he changed was the interface and the result was a massive increase in employee participation.

Making a difference to your employees lives is not necessarily about new and quirky benefits, it’s about inspired HR managers caring about the real issues of their people and trying to make a real difference for them. The benefit package per se is not enough and must be integrated with a communication strategy designed to make employees aware of what is available to them and make sure to design a choice architecture that will favour high participation.

* Financial Well-being: The last taboo of the workplace? Why organisations cannot afford to ignore the financial health of their employees, Douglas Johnson-Poensgen, Barclay’s 2014 # Nudge, Improving decisions about health, wealth and happiness, Thaler & Sustein, Yale University Press, 2008. ^ A Credit union is a non-for-profit organisation that operates savings and loans account for its members. These organisations are fantastic because they provide loans at a fair rate of interest and all the profits are paid back to the members as dividends every year. Some Credit Unions have ties with local employers that they establish on their own or through FairQuid.

Future-proof your employees today and empower them to become Financially Fit!