Debt and fitness are so similar, in many ways.

Almost everyone with debt – not counting mortgages – dreams of being debt free. People who want to get fitter dream of ideal goals and the time when they can walk into a shop, buy what they want and feel amazing.

Both are a lot harder to achieve than dream about.

And even when you are on the road to achieving your goals, there are some times of year when it gets considerably more difficult.

Right now, with Winter setting in and Christmas fast approaching, most people’s diets, credit limits and wallets are going to suffer.

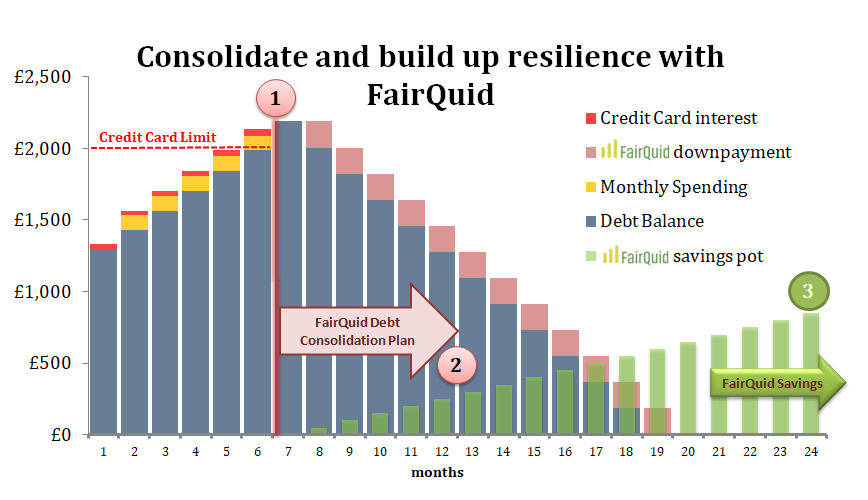

Debt up, savings reduce

Even if you don’t have children, Christmas is an expensive time of year, with presents for families, loved ones, friends and colleagues and dozens of excuses for “treats”, trips away, work meals and parties and nights out chipping away at credit card spending limits, bank accounts and anything you’ve managed to save this year.

Almost everyone puts saving and diets and fitness plans on hold this time of year. Vowing to double-down in January and commit to what you’ve been trying to stick to since earlier this year, maybe even January 2017.

At this time of year, debt levels – which have been rising steadily all year – go up further. Savings, which have been falling all year, reduce further. Low-income families struggle even more, which can be made more difficult if anything unexpected happens, such as a surprisingly high bill or someone loses a job. We’ve seen banks, credit card companies and other lenders take out more and more county court judgements (CCJs) against customers in 2017, which we expect to get worse over the next few months and into next year.

How to start saving and reduce debts

Instead of waiting until January, start solving these problems today.

If you’re in too much debt and want to consolidate, there is a solution.

If you want a little extra money this time of year but you’re worried about your credit rating, we do have an answer.

If you want to start saving, do it now; don’t delay.

With FairQuid Credit Union financial wellbeing solutions, you can consolidate, borrow a little more if needed and start saving today. Providing you’ve been with your current employer at least one year, you can take out a loan with an automatic savings account and payments will come directly from your salary the same day you get paid.

All you need to do is ask your employer to signup to this scheme – it won’t cost them a penny – and our Credit Union partners can offer you a loan with an inbuilt savings account. Eligibility criteria apply. Find out more today.